Merchant-Locked Cards

Merchant Cards lock to the first merchant you make a transaction at.

Single-Use Cards

Single-Use Cards close after the first transaction.

Category Cards

Category-Locked Cards come locked to a predefined merchant category.

Everywhere Cards

Everywhere Cards can be used in-person with mobile wallet compatibility, and don’t lock to a single merchant.

The Best Virtual Card for Business—Top Services Reviewed by Experts

Data breaches are an ever-evolving threat causing major financial repercussions for businesses around the world. According to a 2022 report by IBM, data breaches cost businesses $9.44 million on average. One of the most common reasons behind business security breaches in the U.S. is stolen card credentials.

Using a virtual card for business payments enhances security as the card conceals your company’s financial data and throws malicious actors off the trail. Still, business owners struggle to find a virtual card service that can keep up with their growing needs.

In this guide, we will:

- Explain how virtual cards help businesses

- Review some of the top corporate virtual card solutions

Virtual Cards for Business—An Overview

A virtual card is a unique 16-digit card number with a CVV code and an expiration date designed for secure online payments. Virtual cards can be tied to your bank account or debit or credit card, so you can use your desired funding source for online transactions without revealing your sensitive banking data. A few select providers also offer virtual prepaid cards.

Desired Features of Corporate Virtual Cards

Virtual cards are suitable for both personal and corporate use. If you’re evaluating virtual cards for business use, these are the primary features you should look for:

- Customizable spending limits—A business-friendly card service should have a feature enabling you to set a budget for specific transactions. Virtual cards for employees should have adjustable limits that can be scaled up or down as needed.

- Control options for individual cards—Business owners should be able to close or pause cards to prevent potential misuse and fraudulent activities. Closing the card should not impact the actual bank account or credit line of the user.

- Vendor management—A business should be able to set up multiple virtual cards for different vendors. A merchant-locking feature can help manage this setup. Merchant-locked Cards only work at the designated merchant, allowing the user to track and reconcile merchant payments in a streamlined manner, and categorize expenses (by sorting payments according to nature, such as food delivery, utility services, etc.)

- Fair pricing—Several expensive business virtual card services come with unnecessary features that may not be useful to small-sized businesses. It’s crucial to analyze the company requirements and the price-to-features ratio before committing to a service.

- Ease of use—Virtual card platforms with a difficult setup process or clunky interface will only complicate a company’s daily operations. The ideal service should automate processes like creating cards or completing transactions.

3 Reliable Service Providers for Virtual Corporate Cards

We have presented three virtual card services for business-savvy users. Here’s a summary of our picks, followed by quick reviews:

Before we move on to individual reviews, note that virtual card providers frequently update their products and services. The information in this article is current as of June 2023. Always check the latest terms and conditions of the service before signing up.

Capital One—Virtual Credit Cards for Business

Capital One virtual credit cards are available as an additional service to the bank’s existing credit card customers. For corporate-grade benefits, users typically have to own one of the following Capital One cards[3]:

- Spark® Classic for Business

- Spark Miles for Business

- Spark Cash Select

- Spark Cash Plus

You must have a credit score of 670+ to apply for these cards, which typically come with cashback benefits[1]. Existing cardholders can create virtual card numbers without paying additional fees on the Capital One mobile app or website[4].

The provider offers two types of virtual cards:

- Universal-use virtual cards—Capital One’s universal virtual cards work with almost any online merchant or subscription service[4].

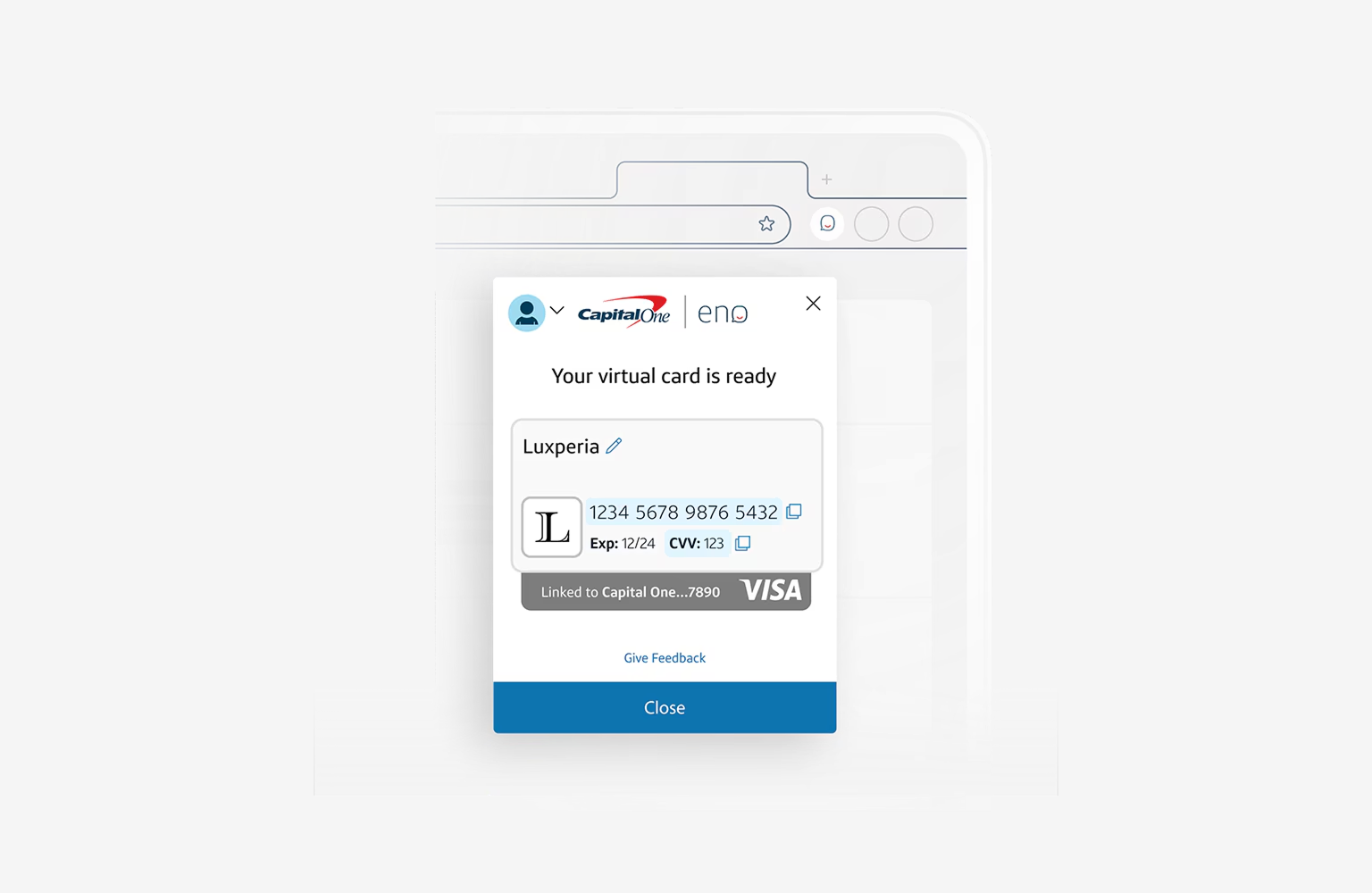

- Virtual cards for specific stores—You can create Capital One’s virtual cards for specific merchants by using the bank’s Eno® browser extension during checkout[4]. Eno saves the card for future purchases at the merchant.

Business Features

Capital One business-use virtual cards/accounts offer the following benefits to users:

- Easy card management—Users can delete, lock, and unlock their virtual cards anytime without affecting the status of their credit card or account.

- Creation of unique employee cards—Capital One business account holders can add employees to their accounts and give them unique Employee Cards for spending. Employee accounts can have customizable budgets[5].

- Centralized monitoring system—Owners can access, review, and print all transactions in their account, whether made by themselves or an employee.

- Fraud protection—Capital One, like many of its competitors in the banking industry, offers $0 fraud liability on both physical and virtual cards[6].

Capital One currently allows the creation of 20 new virtual cards a day, but the option is not available on employee accounts.

It’s important to regularly monitor the Capital One virtual cards you’ve created using the Eno browser extension, especially if a merchant website faces a security breach.

Pros and Cons

Capital One has virtual card features for businesses of all sizes. Since it’s a credit card service, you pay APRs (interest dues) in the range of 17%–30% on all your transactions[7]. If we’re considering downsides, there’s always the looming fear of data breaches with big banks. Over 100 million Capital One customer accounts were compromised in 2019, with sensitive data like Social Security numbers, credit limits, and addresses being exposed.

Here’s a summary of Capital One virtual cards:

Extend—Complementary Corporate Virtual Credit Card Service

Extend is an API-first virtual card platform catering to businesses of all sizes. It is available as a complementary service to business use credit card holders of the following banking partners:

- American Express®

- BMO Financial Group

- Pacific Western Bank

- Regions Bank

- HSBC

- Corpay

- City National Bank

To access the virtual card service, you first need to create a company profile with Extend. Once your account is created, register your eligible commercial credit card with the service and start creating one-time-use or multi-use virtual credit cards. You can create unlimited cards[2].

Business Features

Extend integrates the card creation, distribution, and management process with your existing business system. You can create virtual cards for yourself or send them to employees.

Unlike Capital One, Extend allows setting spending limits for each card[8]. The platform also integrates with Expensify® and Quickbooks® software for easy expense tracking. A unique feature of Extend is that it lets users add notes or attach receipts and invoices to the transactions, which helps with reconciling statements down the line.

Extend virtual cards can be deactivated or reactivated at a user’s convenience[9].

Pros and Cons

Extend is a free-access service with some basic features for business users. Check out its pros and cons:

Privacy—Secure and Versatile Business Virtual Cards

Privacy is a BBB®-accredited independent provider offering virtual cards with multiple business-focused features. The service is bank-agnostic, and you can request a card regardless of your credit score or financial history.

To open a Privacy Virtual Card account, you need a U.S.-based bank account or a bank-linked debit card. Here’s what the signup process looks like for business users:

- Go to the Sign Up page

- Enter the required personal or business information

- Link your bank account

- Request and start creating virtual cards

You can also create a virtual card as a sole proprietor. All you have to do is enter your basic information to verify your identity, as required by law..

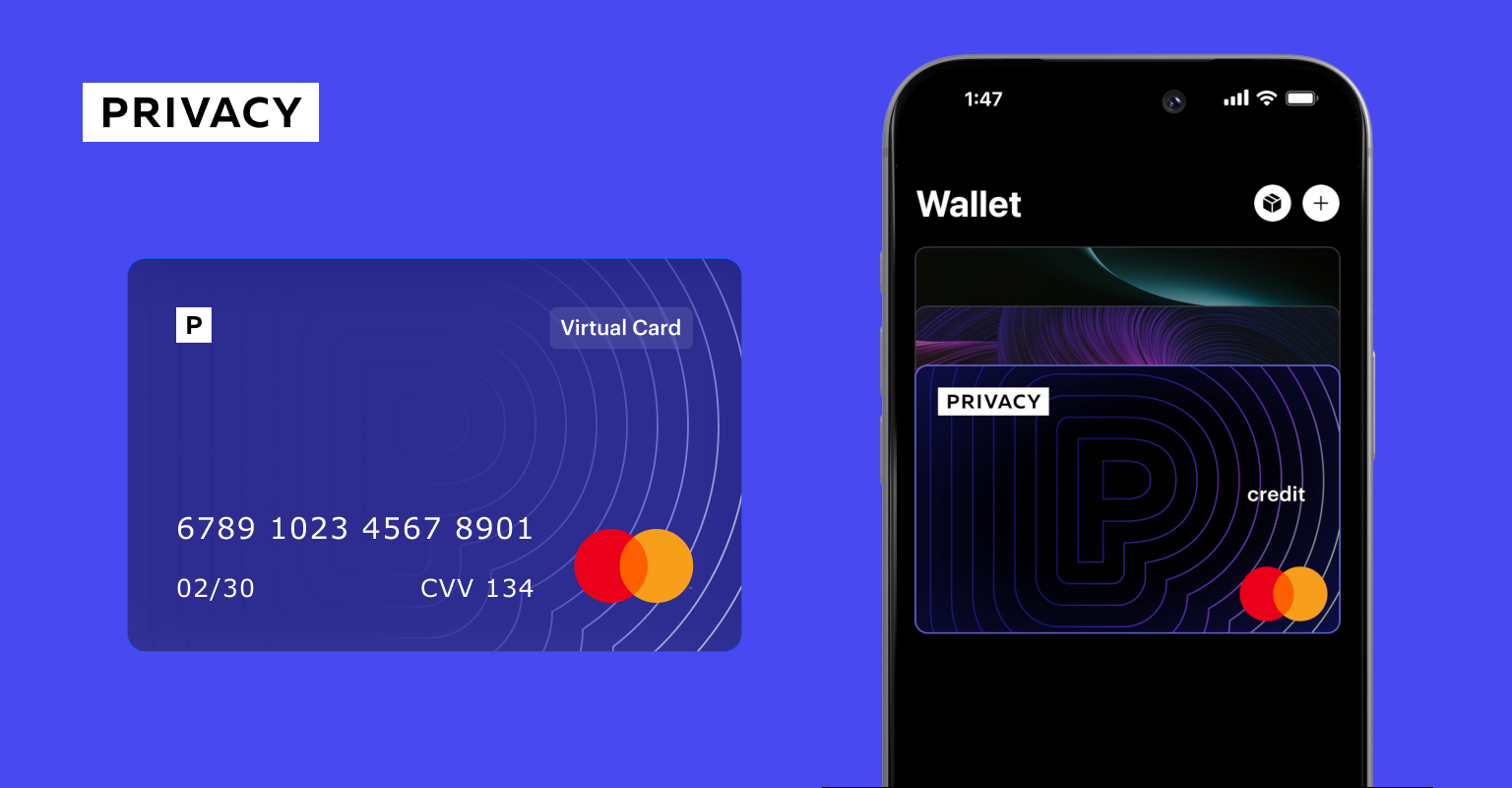

Privacy offers two types of virtual cards:

- Merchant-Locked Cards can be used repeatedly with the same vendor but cannot be used for other merchants. They are ideal for covering everyday products and services (like food deliveries) and paying recurring invoices or subscription charges (like ad service bills).

- Single-Use Cards automatically close immediately after completing a transaction, so you don’t have to worry about manually tracking down and deleting the created cards.

Merchant-Locked and Single-Use Cards have low chances of being misused even if a hacker gets hold of them.

Business Features

Privacy virtual cards have practical business features aimed toward managing everyday expenses and administrative activities efficiently. Some of the standout benefits include:

- Instant checkout with the browser extension—Privacy makes checking out fast and secure with the Google Chrome and Firefox browser extensions. You don’t have to open your Privacy account for every purchase as the extension will create new cards and autofill credentials of your existing ones, minimizing the chances of errors.

- Card sharing with spend limits—Every Privacy Card can be customized with a spending limit, allowing owners to delegate fund accountability tasks to employees. An individual card budget is per transaction, month, or year and can be updated anytime to manage cash flows.

- Individual card controls—You have full control over when to close, pause, and unpause each card. Closing or pausing cards can prevent unwarranted subscription charges from wreaking havoc on your budget. Remember that the option only denies a charge—make sure to reach out to the merchant to cancel the subscription if desired.

- Monitoring and real-time notifications—Privacy users can monitor vendor or employee transaction history on a unified dashboard, accessible on desktop accounts or Android/iOS apps. The platform sends out real-time notifications for every account activity (including declines) to your mobile device or email inbox.

- Free 1Password integration—Business users should not miss out on Privacy’s free 1Password integration service. 1Password is a password manager that allows users to create and manage passwords, tracks data breaches, and monitors password health.

The platform follows PCI-standard security protocols and offers a sophisticated fraud detection system. Sign up for Privacy to access its premium business features.

Pros and Cons

Privacy has emerged as the preferred virtual card solution for businesses. The platform currently offers a base tier that is free for domestic transactions, but businesses should go for the Pro or Premium plan to access benefits like:

- 1% cashback on eligible purchases (totaling up to $4,500 per month)

- Priority support

- Creation of up to 60 new cards each month

Privacy’s incompatibility with credit cards can be an inconvenience for some users, but on the plus side, you avoid the monthly credit card interest payments. Let’s review the pros and cons of Privacy:

Create your Privacy account to explore further.

References

[1] Jeanine Skowronski. Best Capital One Credit Cards. https://www.creditcards.com/capital-one/, May 16, 2023

[2] Extend. https://www.paywithextend.com/faqs, May 2023

[3] Capital One. https://www.capitalone.com/small-business/credit-cards/homepage/, May 2023

[4] Capital One. https://www.capitalone.com/learn-grow/money-management/virtual-cards-shopping-online/, June 23, 2022

[5] Capital One. https://www.capitalone.com/small-business/credit-cards/benefits/employee-cards/, May 2023

[6] Capital One. https://www.capitalone.com/bank/security-fraud-protection/, May 2023

[7] Capital One. https://www.capitalone.com/credit-cards/compare/, May 2023

[8] Extend. https://www.paywithextend.com/virtual-cards, May 2023

[9] Extend. https://support.paywithextend.com/hc/en-us/articles/4405472565783-, May 2023