Cards & Online Payments

Learn everything you need to know about cards and online payments in one place. Discover all the different ways to shop online and how to do so safely.

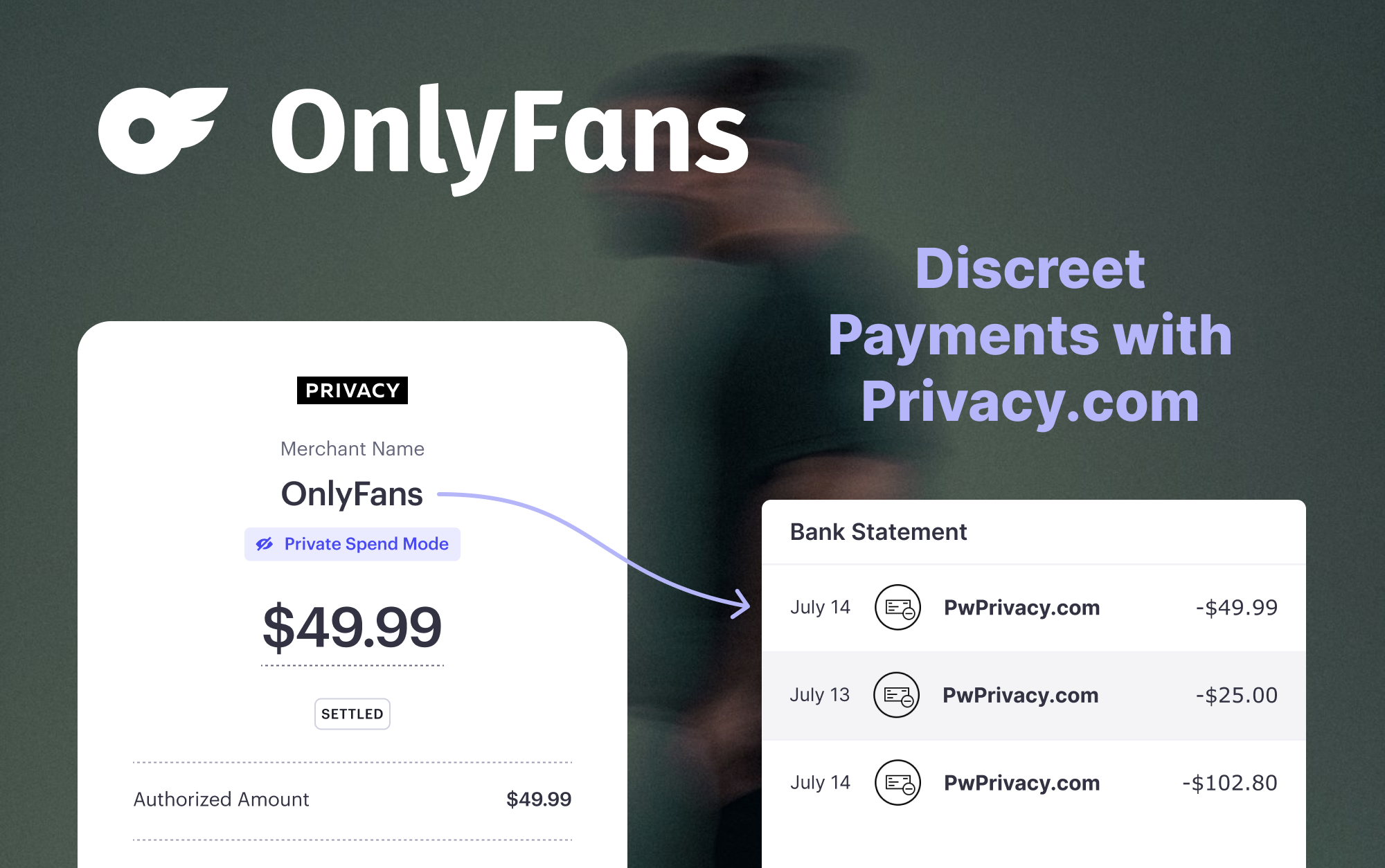

See the best practices for online shopping habits, spending management, and payment security. Learn how to enhance your privacy and financial data security with the help of our detailed guides.